[Good Morning Market] Micron Drops 10%... Korean Stock Market Expected to Open Weak

Philadelphia Semiconductor Index Down 6.3%

"KOSPI Momentum Remains Intact... Fund Flows Expected to Rotate into Other Sectors"

As the New York stock market closed lower across the board due to weakness in the semiconductor sector, the Korean stock market is expected to start on a weaker note on July 2, 2026.

On July 1 (local time) at the New York Stock Exchange (NYSE), the Dow Jones Industrial Average finished at 52,305.24, down 13.96 points (0.03%) from the previous trading day. The S&P 500 index, which focuses on large-cap stocks, fell by 16.13 points (0.22%) to 7,483.23, while the Nasdaq index, which is centered on technology stocks, ended at 26,040.03, down 173.68 points (0.66%).

In particular, the Philadelphia Semiconductor Index dropped by 6.3%. Broadcom fell by 2.23%, Micron by 10.57%, SanDisk by 10.62%, Nvidia by 1.25%, Intel by 9.03%, Qualcomm by 1.55%, AMD by 6.89%, and Broadcom by 2.23%, all closing lower.

A trader is working at the New York Stock Exchange in the United States. Photo by Getty Images Yonhap News.

View original imageNews that Meta will enter the cloud business by leveraging surplus artificial intelligence (AI) computing power triggered the decline in the indices.

Ji-Young Han, a researcher at Kiwoom Securities, said, "Meta has been one of the hyperscalers driving the AI investment cycle, leading to higher memory prices and improved performance in semiconductor stocks. The fact that they may shift from being a buyer to a seller of computing power suggests that current demand may not be sufficient for the massive investments made, leading to market concerns."

She added, "However, the sharp drop in semiconductor stocks is largely due to profit-taking pressure, as fatigue has accumulated after record-high gains in the second quarter, and the news of Meta's entry into the cloud business acted as a catalyst."

Kevin Warsh, Chair of the Federal Reserve, also influenced the market by stating at the European Central Bank (ECB) that "expected inflation has declined." He emphasized that although U.S. President Donald Trump has been pressuring for interest rate cuts, monetary policy decisions will remain independent of political pressure. He also commented on the current price levels, saying, "If you look around, you can see that prices are too high."

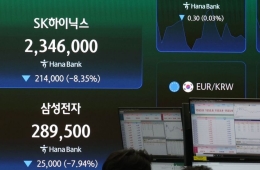

Regarding the Korean stock market, the researcher said, "The sharp drop of over 6% in the Philadelphia Semiconductor Index is expected to exert downward pressure on domestic semiconductor stocks, leading to a weak start." She also noted, "The recent surge in KOSPI volatility, mainly driven by semiconductor stocks, could make the market more sensitive to negative rather than positive factors."

A dealer is working in the dealing room of Hana Bank in Jung-gu, Seoul, on the 1st as the KOSPI closed the session down over 2% in the 8,300 range. Photo by Yonhap News Agency

View original imageNonetheless, she emphasized, "The second-quarter earnings momentum for the KOSPI remains intact," adding, "It is worth noting that as a counterbalance to the prolonged focus on semiconductors, there is now a rotation into other sectors such as electric equipment, defense, and bio, which have seen their stock prices suppressed for a long time."

Hot Picks Today

![JoongAng Ilbo Resorts to Selling Management Rights: The Reason Behind It [Why&Next]](https://cwcontent.asiae.co.kr/asiaresize/93/2026070208343431191_1782948874.png) JoongAng Ilbo Resorts to Selling Management Rights: The Reason Behind It [Why&Next]

JoongAng Ilbo Resorts to Selling Management Rights: The Reason Behind It [Why&Next]

- "Now Is Not the Time to Sell, Buy More on Sharp Declines"... Advice Amid Market Volatility

- "An 'Easy Group' but Early Exit: Japanese Media Names South Korea Among 'Worst Teams of the World Cup'"

- "Why Did You Call Me to the World Cup!" Jens-Hong Myung-bo Assault Video Surpasses 10 Million Views... Revealed as AI

- Suspicious Achievements of Famous 'Beauty' Policewoman Revealed to Be Handed Over by Male Colleagues... Taiwan in Shock

The researcher further explained, "Compared to the period from May to mid-June, the burden on valuations in non-semiconductor sectors, caused by U.S. market interest rates, is also easing. Even if weakness in semiconductors emerges today, the index is likely to be supported as funds are redistributed into other sectors, rather than a broad outflow from the overall market."

© The Asia Business Daily. All rights reserved. Unauthorized AI training and use prohibited.