Wall Street Lowers the Bar for Index Inclusion to Add SpaceX and OpenAI

As the likelihood of IPOs by major unlisted companies such as SpaceX, OpenAI, and Anthropic increases, major index providers are moving to revise their inclusion rules, such as profitability requirements and waiting periods. This move is intended to reflect these companies in indexes more quickly, given their significant potential impact on the market after listing. However, concerns have been raised that making exceptions only for large IPOs could undermine the neutrality of the indexes and automatically expose investors to overvalued and low-liquidity stocks.

According to the Wall Street Journal (WSJ) and Bloomberg on the 3rd (local time), S&P has recently begun soliciting opinions on amending its rules so that mega-cap companies pursuing IPOs can be included in key indexes, such as the S&P 500, more quickly.

The proposed rule change shortens the minimum period a company must be publicly traded to qualify for index inclusion from the current 12 months to 6 months. In addition, S&P is also considering waiving profitability and liquidity requirements for large companies.

The comment period will run until the 28th of this month. If the changes are finalized, they are scheduled to take effect before the market opens on the 8th of next month. Bloomberg reported that this timeline precedes the anticipated IPO of SpaceX at the end of June, as well as the potential listings of OpenAI and Anthropic. If the proposed changes are approved, SpaceX, along with OpenAI and Anthropic when they go public, may be included in the S&P 500 more quickly.

Nasdaq has also revised its rules to allow large-cap stocks that meet certain criteria to be more swiftly included in the Nasdaq 100 index. Under the new rules, IPO stocks that rank within the top 40 by market capitalization can undergo an evaluation on the seventh trading day after listing and may be included in the index typically 15 trading days after their debut. Previously, a minimum trading period of three months was generally required after listing.

However, some critics argue that these measures amount to relaxing existing principles simply to include popular companies like SpaceX and OpenAI in the indexes sooner. While index providers explain that these changes are designed to timely reflect mega-IPOs, the WSJ points out that, in reality, they are moves to more quickly include 'hot stocks' that investors desire. There are also concerns about fairness, as S&P is seeking to waive profitability requirements for IPO companies large enough to rank in the top 100 by market cap, but intends to maintain these requirements for other companies.

Profitability requirements and post-listing waiting periods have traditionally served as safeguards to prevent loss-making companies or newly listed firms with high price volatility from being included in indexes without sufficient scrutiny. If such standards are relaxed for mega-cap companies, index inclusion could precede adequate market validation of a company's value.

Hot Picks Today

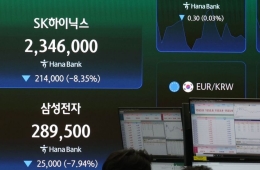

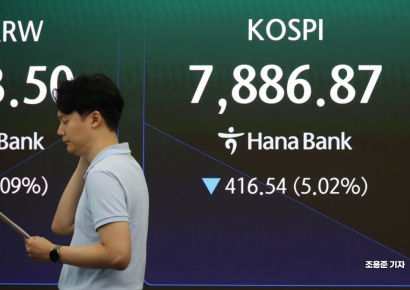

"Semiconductor Peak-Out Theory Resurfaces: Foreign Investors' KRW 3.2 Trillion Net Sell Pushes KOSPI Below 8,000"

"Semiconductor Peak-Out Theory Resurfaces: Foreign Investors' KRW 3.2 Trillion Net Sell Pushes KOSPI Below 8,000"

- [Exclusive] "Tens of Billions Paid": Unregulated Bonuses for Union Presidents Spark Controversy... Ministry of Land Launches Nationwide Investigation

- "Now Is Not the Time to Sell, Buy More on Sharp Declines"... Advice Amid Market Volatility

- "Should I Send My Sons to Paichai High?" Swimmer Heeyeon Jo Stirs Debate With Post Amid Cheering Chant Controversy

- Suspicious Achievements of Famous 'Beauty' Policewoman Revealed to Be Handed Over by Male Colleagues... Taiwan in Shock

Additionally, since inclusion in an index immediately triggers capital inflows through funds and ETFs that track the index, there are concerns that this could drive up stock prices before proper price discovery takes place. George Noble, Chief Investment Officer (CIO) of Noble Capital Advisors, criticized Nasdaq's rule changes in an interview with U.S. economic media outlet Kiplinger, calling them "the most blatant example of structural manipulation ever seen in a major index." He noted, "The advantage of indexing was that it could free-ride on the price discovery performed by active managers," and added, "Now, the index itself has become the market."

© The Asia Business Daily. All rights reserved. Unauthorized AI training and use prohibited.