[The Fifth Generation of Private Health Insurance Is Coming]②The High-Stakes Gamble of Reform... Financial Authorities to Announce 'Buyback and Optional Rider' Plan Next Month

16 Million Legacy Policyholders... Will Incentives Work?

Accelerating Uninsured Coverage Reforms... Can the Vicious Cycle of Loss Ratios Be Broken?

Incentives Key to Driving Switches... Industry Calls for Easing Premium Regulations

The insurance industry believes the success or failure of the fifth-generation indemnity insurance reform will ultimately depend on how many existing policyholders switch to the new generation. However, it is pointed out that strong incentives, such as premium discounts, are essential to motivate those wishing to keep their current plans. In response, the financial authorities plan to announce a new reform package for indemnity insurance next month, including measures like "contract buybacks" and "optional riders."

![[The Fifth Generation of Private Health Insurance Is Coming]②The High-Stakes Gamble of Reform... Financial Authorities to Announce 'Buyback and Optional Rider' Plan Next Month](http://www.asiae.co.kr/news/img_view.htm?img=2026040907181418745_1775686695.png)

The Key to the Indemnity Insurance Reform Is “Switching”... Authorities Present 'Buyback and Optional Rider' Solutions

According to the Financial Services Commission and other sources on April 9, the financial authorities are working with the industry to announce a reform package for indemnity insurance—including contract buybacks and optional riders—early next month. “Contract buyback” refers to insurers purchasing existing indemnity policies from policyholders. The authorities are reportedly considering a plan to offer a 50% premium discount for three years to policyholders of first- and early second-generation indemnity insurance who switch to a fifth-generation product. The number of policyholders eligible for contract buybacks is estimated at around 15.82 million.

However, the industry is pushing back, arguing that implementation costs would reach several trillion won and that there are fairness issues with those who have already switched, making the proposal unrealistic. Nevertheless, the authorities believe that the first- and second-generation indemnity insurance products were designed without sufficiently factoring in the scale of losses, resulting in continued deterioration of the loss ratio. According to the Insurance Research Institute, the risk loss ratio for first to fourth-generation indemnity insurance stood at 119.3% as of the third quarter of last year. This means that for every 10 billion won received in premiums, about 11.93 billion won was paid out. The authorities’ position is that, even if it requires bearing significant costs, such reforms are necessary to improve this structure. So-called “medical shopping” not only leads to insurance payout leaks, but also worsens the finances of the national health insurance program.

To further encourage policyholders of older products to switch, the authorities are also considering “optional riders.” This was a campaign pledge by President Lee Jae-myung during his candidacy. The system was initially considered for introduction in June last year, but the schedule was repeatedly delayed due to industry disagreements and regulatory design challenges. Although it was expected to be introduced in the second half of this year, the announcement has now been moved forward. The authorities’ rush to introduce optional riders appears aimed at minimizing coverage gaps caused by the timing difference with the introduction of “managed benefits.” The Ministry of Health and Welfare is targeting the third quarter of this year for the introduction of managed benefits.

Optional riders allow policyholders to lower their premiums in exchange for decreasing coverage on certain non-insured items—such as manual therapy—or increasing their own share of the costs. The financial authorities have already collected industry feedback, and it is understood that instead of adopting an entirely new structure, they are reviewing improvements based on the third-generation indemnity insurance system, which separates insured and non-insured benefits.

As a result, the core insured benefits will be maintained, but the authorities are likely to adjust the riders focused on the so-called “three major non-insured items”—MRI scans, manual therapy, and injections—by either narrowing the scope of coverage or increasing the policyholder’s share of costs.

Last year, the five largest non-life insurers in Korea (Meritz, Samsung, Hyundai, KB, and DB) paid out a total of approximately 10.9779 trillion won in insurance claims. Of this, about 1.8701 trillion won was related to physical therapy (including manual therapy, extracorporeal shock wave therapy, and proliferative therapy), while non-insured injections (such as nutritional injections) accounted for about 726.6 billion won. Together, these two categories made up roughly a quarter of the total insurance payouts.

An official from the Financial Services Commission stated, “While the policy will be announced next month, actual implementation will take some time. Since preparation is needed, including the construction of IT systems, we are considering announcing the policy direction first and deferring the implementation date.”

![[The Fifth Generation of Private Health Insurance Is Coming]②The High-Stakes Gamble of Reform... Financial Authorities to Announce 'Buyback and Optional Rider' Plan Next Month](http://www.asiae.co.kr/news/img_view.htm?img=2026040907182818747_1775686709.png)

The Conversion Rate Will Decide Success... Despite Incentives, 16 Million Existing Policyholders “Holding Out”

The financial authorities’ “carrot” measures are seen as an effort to encourage existing policyholders to switch. Currently, about 16 million people—roughly 44% of all indemnity insurance policyholders—still hold first- and early second-generation products.

![[The Fifth Generation of Private Health Insurance Is Coming]②The High-Stakes Gamble of Reform... Financial Authorities to Announce 'Buyback and Optional Rider' Plan Next Month](http://www.asiae.co.kr/news/img_view.htm?img=2026040914453119963_1775713530.png)

This is due to the extremely generous coverage conditions of those products. First- and second-generation indemnity insurance offers virtually unlimited coverage on non-insured services and no renewal cycles, meaning there is little risk of reduced coverage in the future. Even items subject to controversy over overtreatment—such as manual therapy and non-insured injections—are broadly covered. From the policyholder’s perspective, there is little incentive to cancel their existing contract and switch to a new product.

The key issue is whether the government’s incentives can persuade existing policyholders to switch. The industry expects the number of first- and second-generation policyholders switching to fifth-generation products will fall short of expectations. Past trends support this outlook. According to the General Insurance Association of Korea, the number of policyholders switching from the first, second, and third generations to the fourth generation surged from 104,794 in the second half of 2021 to 568,362 in 2022, peaking at 671,657 in 2023. However, the figure dropped to 564,796 in 2024 and 378,584 in 2025.

Hot Picks Today

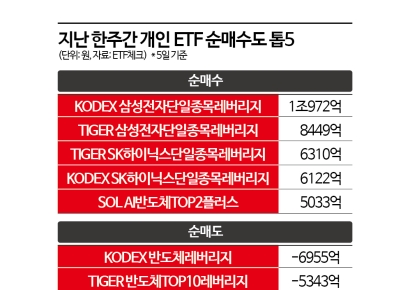

"Let's Double with Samsung and SK hynix": Retail Investors Dump Semiconductor ETFs for Samsung and SK hynix Leverage Products

"Let's Double with Samsung and SK hynix": Retail Investors Dump Semiconductor ETFs for Samsung and SK hynix Leverage Products

- "Why Is There No Substitute Holiday for Memorial Day?"... Here's Why

- [Column] Court Dismisses HD Hyundai Heavy Industries' Injunction Over 'Security Penalty' in KDDX Bidding War

- Waking Up to 33 Trillion Won in His Account... Bank Staff Say "Unbelievable"

- "The Only One in the World... Worth 1.5 Billion Won" The Recipient of Jensen Huang's Gifted Graphics Card Is

Since contract buybacks are not mandatory, some argue that insurance companies will need additional support—such as relaxed regulations on premium increases—to actively promote them. Under the current supervisory regulations, indemnity insurance premiums can only be raised by up to 25% per year. An official from a non-life insurance company said, “Incentive measures such as premium discounts were behind the surge in switchovers at certain times. If the contract buyback price is determined by the difference between premiums and insurance payouts, the cap on premium increases should be eased at the very least, and we have conveyed this opinion to the Financial Services Commission.”

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

!["Don't Get Excited, Crushes Are Exhausting Too: Even Unrequited Love Faces a Recession [World is Z Gold]"](https://cwcontent.asiae.co.kr/asiaresize/307/2026060508335888548_1780616038.png)