Corporate Governance Reforms and Hong Kong ELS Sanctions... A Watershed Moment for Banks in March

Outline of governance overhaul and ELS penalties expected next month

CEO liability likely to expand in cases of internal control failures

Stronger household debt controls to intensify pressure on profitability

With final decisions on the restructuring of bank governance and the imposition of fines related to the mis-selling of equity-linked securities (ELS) tied to the Hang Seng China Enterprises Index (HSCEI) in Hong Kong scheduled for next month, tension is mounting in the banking sector. As financial authorities emphasize the responsibility for internal controls and consumer protection, and as the trend toward strengthening household loan management is materializing, it is expected that banks will be compelled to revise their strategies regarding both governance and overall profitability.

According to the financial sector on February 27, the Financial Services Commission is set to finalize the amount of fines related to the mis-selling of Hong Kong H-Index ELS in the banking sector next month, following deliberations by the Agenda Review Subcommittee and a regular meeting. Although it was initially expected that the Securities and Futures Commission would determine the fines, the decision-making process was transferred to the Subcommittee and regular meeting as no conclusion was reached.

The primary concern for banks is the size of the fines. Previously, the Sanctions Review Committee of the Financial Supervisory Service reduced the initial fine, which was about 2 trillion won, to approximately 1.4 trillion won. As a result, the fine for KB Kookmin Bank, originally around 1 trillion won, was lowered to the 800 billion won range, while the fines for Hana Bank and Shinhan Bank, both previously around 300 billion won, were each reduced to the 200 billion won range. NH Nonghyup Bank and SC First Bank, which were facing fines in the 100 billion won range, reportedly saw reductions of about 15% to 20% as well.

The banks are hoping for further reductions, given that they have already completed voluntary compensation of about 1.3 trillion won to more than 90% of affected customers. Under the current Financial Consumer Protection Act, if post-incident recovery efforts are recognized, fines can be reduced by up to 50% as a rule. If additional requirements are met, the reduction can extend up to 75%. Banks have expressed hope that the maximum 75% reduction will be applied.

The scale of the fines is expected to inevitably affect the banks' performance this year. Since fines are treated as expenses, there is a strong possibility that net profit will decrease. In fact, KB Financial Group's net profit for the fourth quarter of last year fell by 57.2% quarter-on-quarter, impacted by one-off factors such as the provision for ELS-related fines. As of the end of last year, KB Kookmin Bank had set aside 263.3 billion won in provisions for Hong Kong ELS fines. If the fine is finalized in the 800 billion won range without further reduction, the bank will have to set aside an additional 500 billion won or more in provisions.

An official at a commercial bank stated, "In the case of ELS, after the final decision is made at the Financial Services Commission's regular meeting, follow-up measures such as additional provisioning will be taken if necessary."

The governance restructuring is also expected to place a significant burden on bank management. Financial authorities have established a task force to advance governance, pushing for institutional improvements such as strengthening the responsibilities of the board of directors and codifying the CEO's obligations for internal control. Lee Chanjin, Governor of the Financial Supervisory Service, emphasized that these are "directions that must be adhered to regardless of the implementation timeline," placing pressure on banks to respond proactively. As this governance reform is being perceived as a call for actual changes in management practices rather than a mere recommendation, analysts believe that banks will inevitably have to revise their internal control strategies.

The financial authorities' policy stance of strengthening household loan management is another source of pressure. At the end of last month, the Financial Services Commission announced that it is considering managing this year's target growth rate for household loans in the banking sector at a lower level than last year's 1.8%. The household debt management plan to be announced next month is expected to include additional measures such as stricter regulations on loan maturity extensions for multiple homeowners and landlords, and separate management of aggregate limits for mortgage loans. If total lending limits are tightened, banks will inevitably see a slowdown in loan growth, which is likely to lead to a decrease in interest income—a core source of profit.

Hot Picks Today

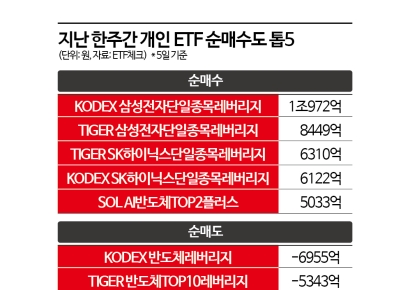

"Let's Double with Samsung and SK hynix": Retail Investors Dump Semiconductor ETFs for Samsung and SK hynix Leverage Products

"Let's Double with Samsung and SK hynix": Retail Investors Dump Semiconductor ETFs for Samsung and SK hynix Leverage Products

- "Extremely Undervalued Range" Despite Record-Breaking Results, This Sector Nears New Lows [Weekend Money]

- "Why Is There No Substitute Holiday for Memorial Day?"... Here's Why

- Paid 180,000 Won as Wedding Gift but Only Got Cold Burgers... "Is This a Cash Grab at a Wedding?"

- The Ice Cream You Asked Friends to Bring Back Is Now a Hit: Over 30 Billion Won Sold in the U.S. Alone

Another bank official said, "As the strengthening of governance responsibilities coincides with tighter total household loan regulations, banks will have no choice but to readjust their overall management strategies. This will likely accelerate efforts to restructure their profit portfolios, including the expansion of non-interest income."

© The Asia Business Daily(www.asiae.co.kr). All rights reserved.

!["Don't Get Excited, Crushes Are Exhausting Too: Even Unrequited Love Faces a Recession [World is Z Gold]"](https://cwcontent.asiae.co.kr/asiaresize/307/2026060508335888548_1780616038.png)